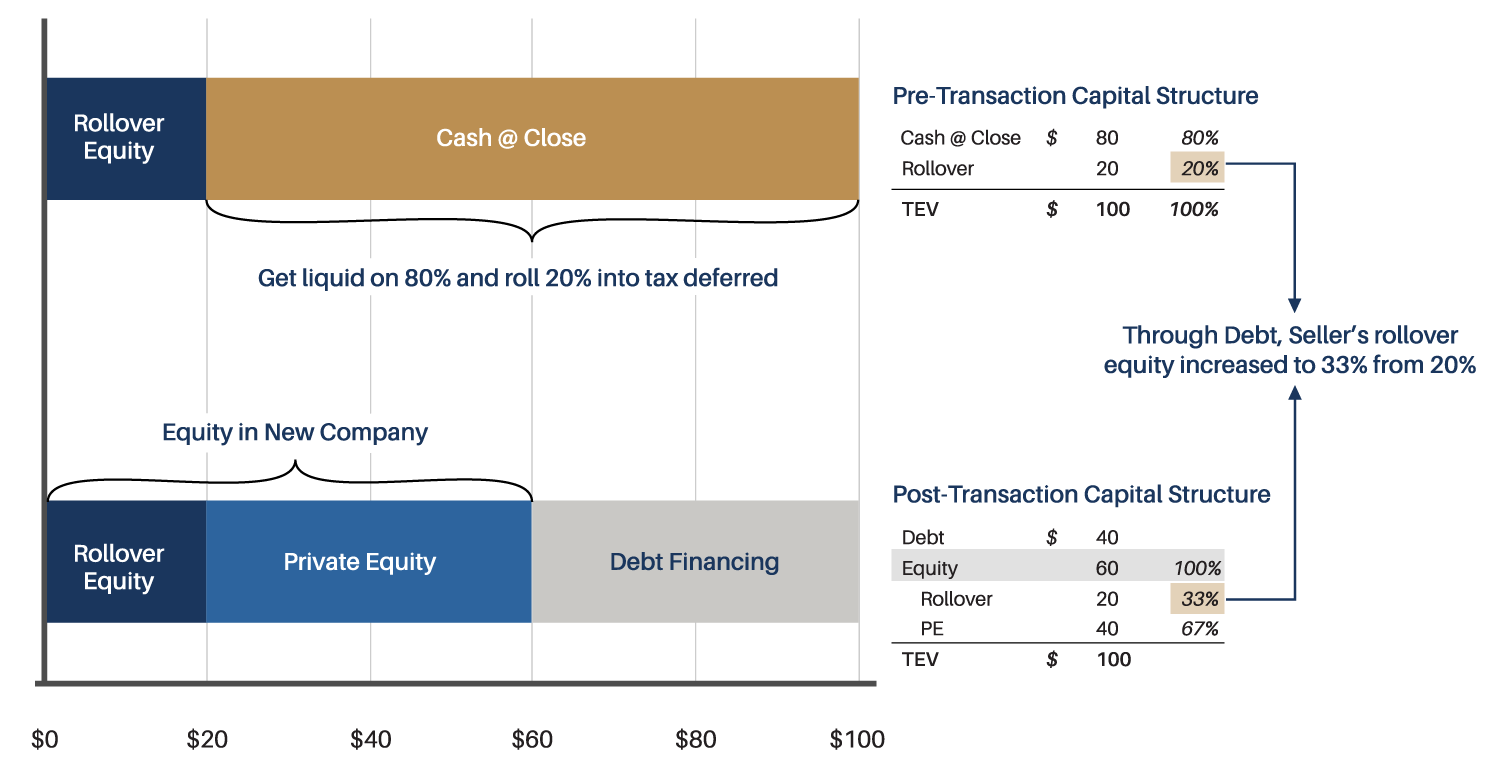

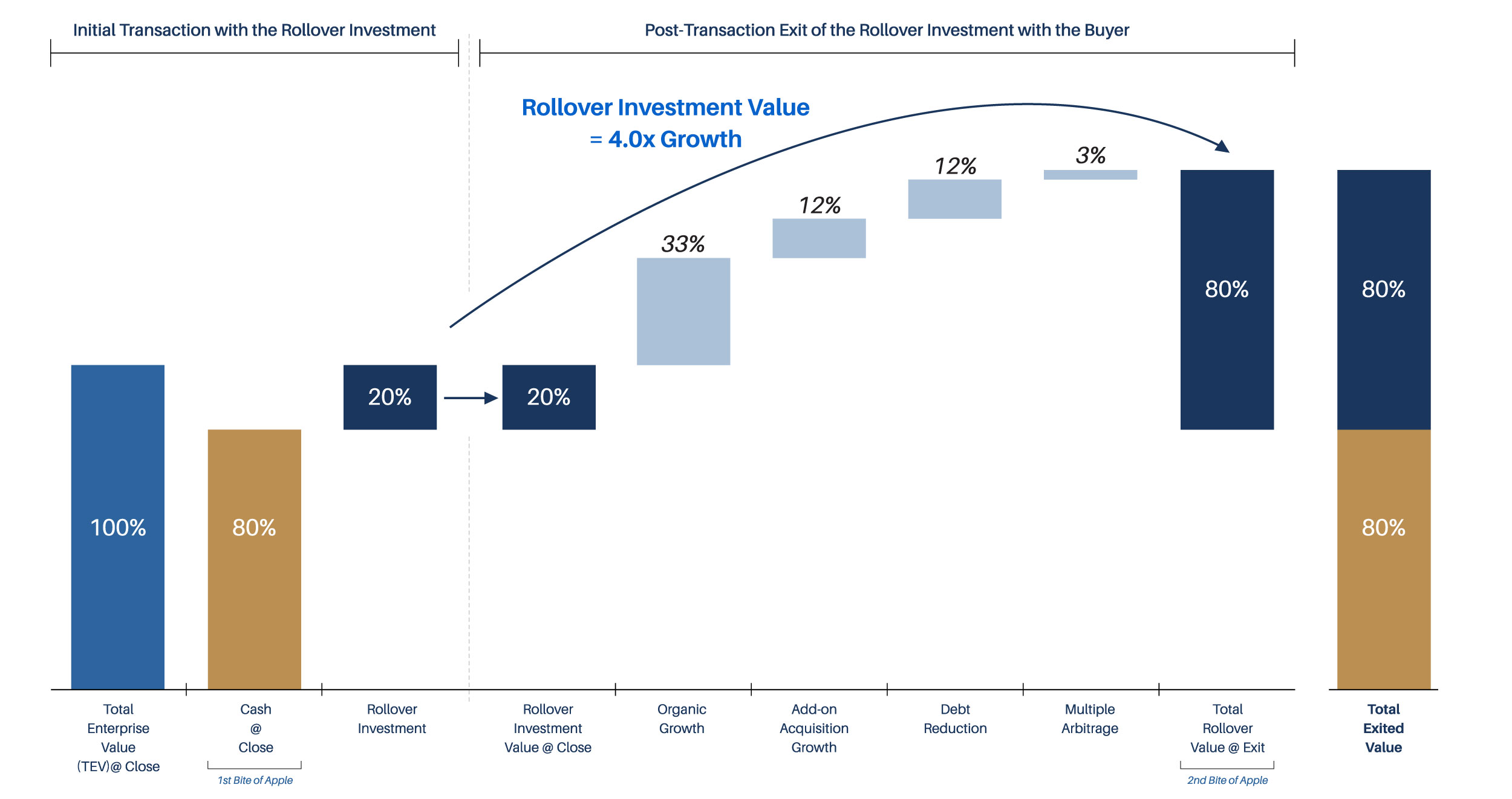

In a majority recapitalization, ownership sells a majority of interest in their company to an investor while maintaining a minority position and continuing to work for the company post transaction. To better illustrate, an owner would like to diversify their net worth and bring on a financial partner to help aggressively grow their business. Ownership is still engaged in the business, recognizes the potential for growth, and would like to maintain a level of exposure to the upside. In this example, the owner chooses to liquidate 80% of their ownership in the company while retaining exposure to 33% of the company moving forward, satisfying both near- and long-term objectives.

Strong buyers are committed partners, focused on adding value to what you have already created by leveraging their considerable managerial experience, operational knowledge, customer strategies, and industry relationships to help strengthen the growth of your business. With thoughtful acquisitions and a robust, organic growth plan, your business can scale and realize the full upside potential of growth.

Private equity is seeking platforms with best-in-class leadership and the business platform to serve as the support for a combined organic and inorganic (acquisitive) growth strategy.

Private Equity does NOT interfere with or run company operations. The existing leadership runs the show. The primary difference is that leadership is now equipped with a resourceful partner that can strengthen the development of the next phase of the business.

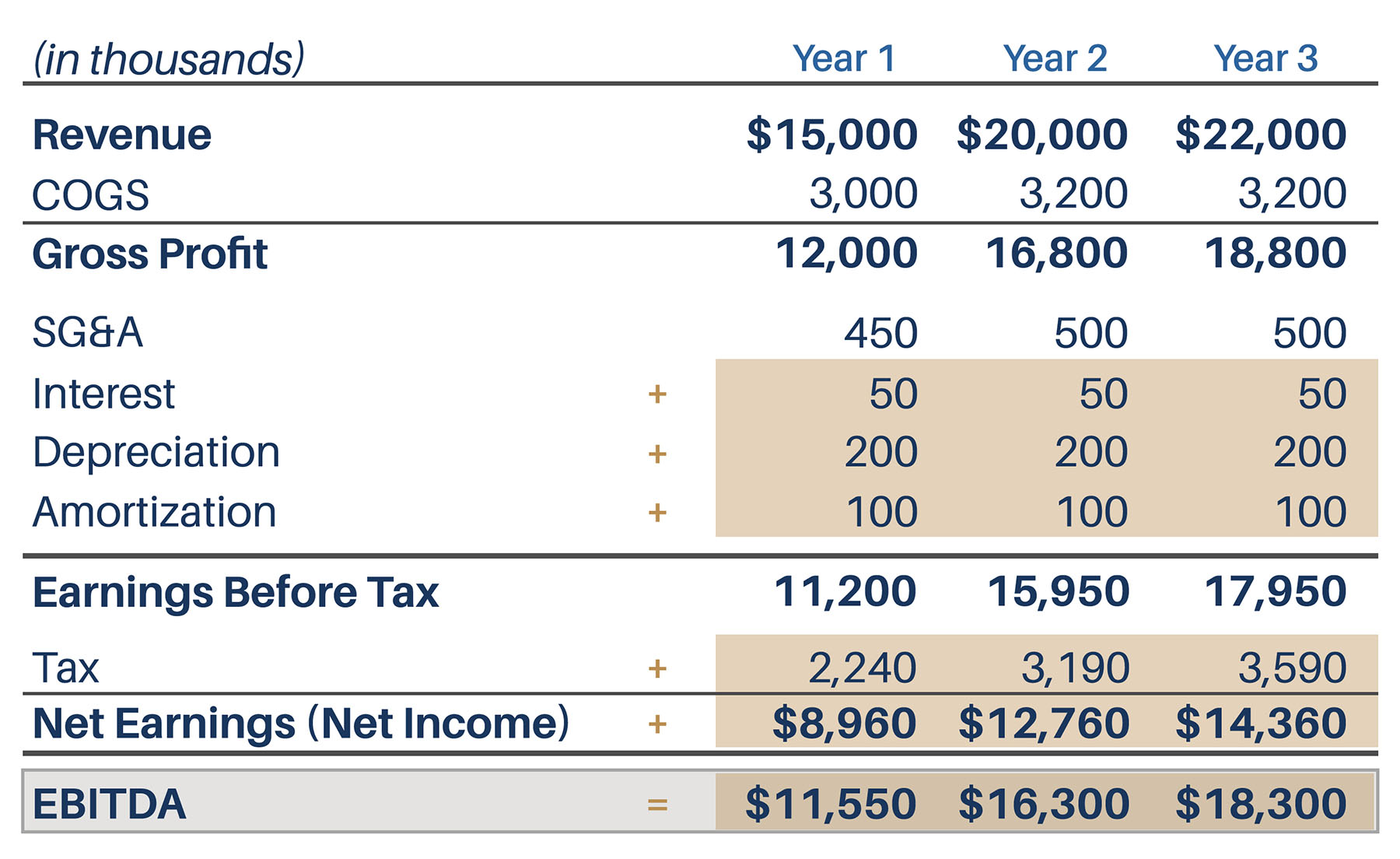

In the world of Mergers & Acquisitions, the value of a private Company is typically based on EBITDA.

EBITDA stands for “Earnings Before Interest, Taxes, Depreciation and Amortization.” EBITDA is a metric used to evaluate a company’s operating performance. It can be seen as a proxy for cash flow from the entire company’s operations.

EBITDA = Net Income + Taxes + Interest Expense + Depreciation + Amortization

It is usual that the Company identifies additional expenses (“Adjustments”) to be included as part of EBITDA to better represent the true operating base of the business. Adjustments to EBITDA can vary widely between industry and company. The following items are commonly adjusted.

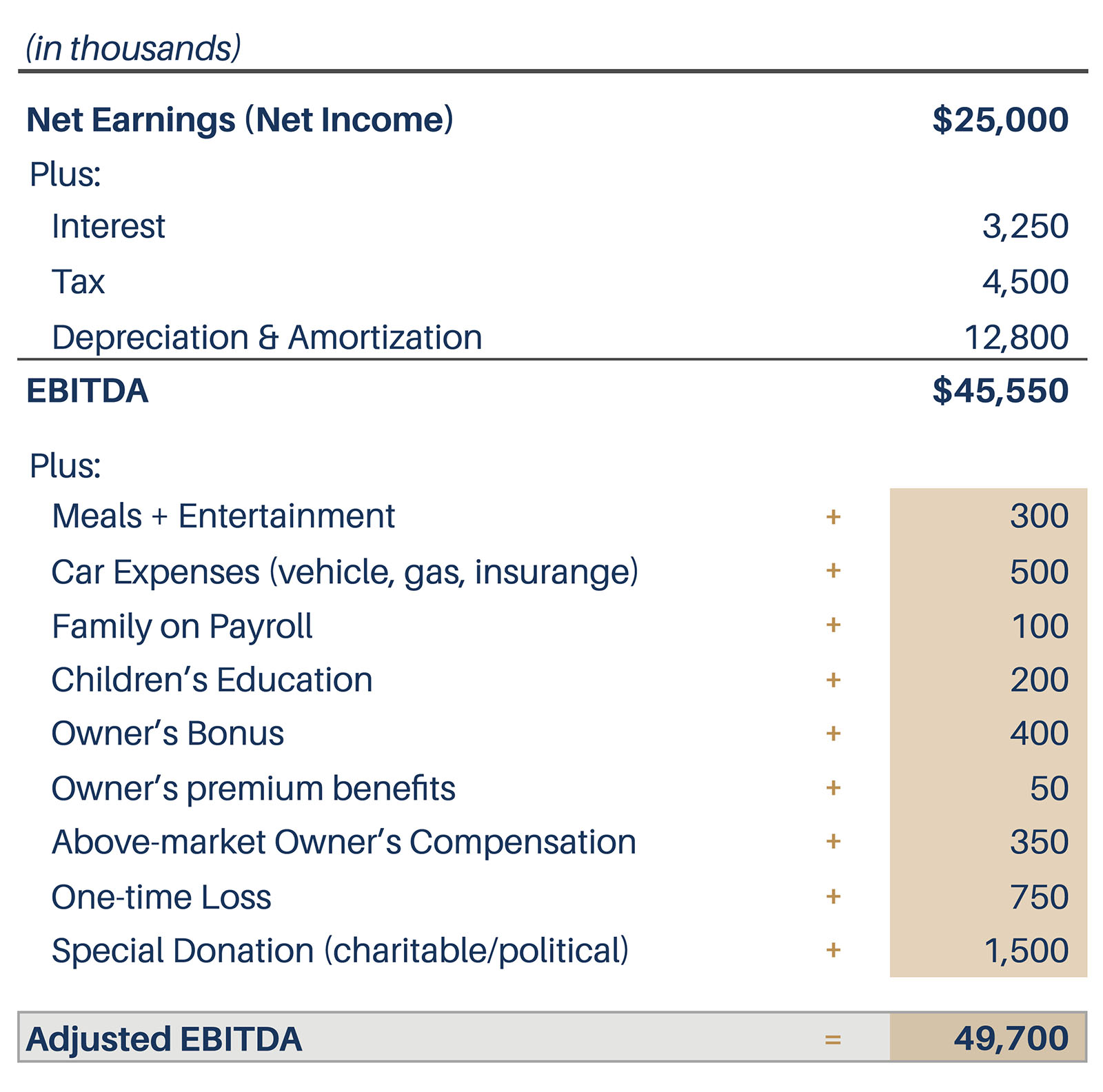

An Example:

To calculate Adjusted EBITDA, we first calculate the unadjusted EBITDA. We start by taking net income and adding back interest, taxes, depreciation and amortization. Using an example income statement, we start with the net income of $25,000,000 and add back taxes, interest expense, and depreciation & amortization. The resulting EBITDA is now calculated at $45,550,000.

Next, we move to the adjusted EBITDA by identifying adjustments. In the example, we identify adjustments that total $4,150,000. Anything that is non-recurring, extraordinary, or personal in nature will be added back to arrive at what the true Free Cast Flow (FCF) of the business would be if the buyer were to own it. Added to EBITDA, the adjusted EBITDA has been calculated at $49,700,000, a significant difference between the net income of $25,000,000.

Interest is included in EBITDA as it depends on the financing structure of a company. Interest comes from the money the company has borrowed to fund business activities. Different companies have different capital structures, resulting in different interest expenses. Hence, it is easier to compare the relative performance of companies by adding back interest and removing the impact of capital structure on the business.

Taxes vary based on the region where the business is operating. Taxes are a function of tax rules, which are not part of assessing a management team’s performance. Thus, financial analysts prefer to add them back when comparing businesses.

Depreciation and Amortization (D&A) depend on the historical investments the company has made and not on the current operating performance of the business. Companies invest in long-term fixed assets (such as buildings or vehicles) that lose value due to wear and tear. The depreciation expense is based on a portion of the company’s tangible fixed assets deteriorating. The amortization expense is incurred if the asset is intangible. Intangible assets, such as patents, are amortized because they have a limited useful life before expiration (competitive protection). D&A is heavily influenced by assumptions regarding useful economic life, salvage value, and the depreciation method used. Because of this, analysts may find that operating income is different than what they think the number should be, and therefore D&A is backed out of the EBITDA.